Artificial Intelligence has transformed the world of finance. AI has completely revamped Loan Approvals and Scoring Credit forms. Until recent times, it was consuming a huge amount of time as it required paper work. Artificial Intelligence has ensured that such tasks are not only completed robustly but also much more accurately and also much speedier. Let us see how AI provides solutions for borrowers and lenders.

A New Route to Credit Scoring

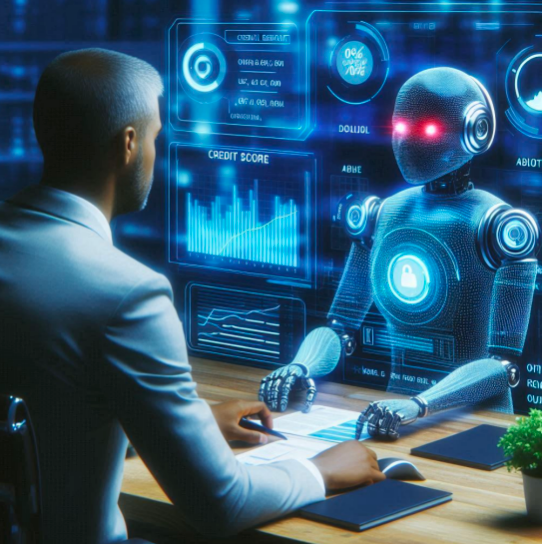

Traditional credit score system are outdated now after emergence of AI. Previous credit scoring contains information on your pay history, length of time you have had credit and debt that you owe. It is a model that applies to the majority of the borrowers, though it is somewhat inconsistent in a way that many borrowers cannot even qualify for the loan because they don't have sufficient prior credit.

Lending is being revolutionized by Artificial Intelligence. It is not taking money-profiles of your borrowing habits but also collects and analyzes much more data about you. Such AI-based systems can review your utility payments and even scrutinize your behavior on the World Wide Web as well as social media use. With all your credible sources of information, AI can pull a more well-rounded picture of you for lenders to view. A McKinsey study in 2022 indicates AI-led underwriting increases the purchase of loans by 20%. It reduces the default rate by 10%. In a nutshell, those who could not qualify for loans under the old system should find their luck has improved.

Much Quicker and More Accurate Loan Approvals

One interesting aspect about AI is that it performs at such a speed relative to the traditional system that took so long of waiting time. With AI, a lender can look at massive amounts of data and make a decision in real-time. In this way both lenders and also borrower benefit from this of making decisions.

AI credit rating system keeps on learning from past decisions and can identify loan agreements that that are untraceable by the traditional credit rating system. A Forbes article found out that by 2023, AI has reduced total time to approve loans by 50% as well as cut human error by another 35%. Even quicker decisions have been taken to lower costs and greater customer satisfaction to lenders.

Personalized Loan Offers

This point, where AI does not necessarily hasten the decisions by lenders alone, makes them personalized. This means if you have a willingness to borrow, it will be within your bank's power to rely on its AI system to pinpoint the appropriate loan products that may align with your financial habits or personal objectives at hand. Their intention is to make the loan experience more personalized towards helping you have more relevance with it. Its aim is also to give you a better opportunity for having your request funded.

This also caters to individuals who are devoid of traditional credit. According to Zest AI-an AI-driven loans approval has grown to 15% more in underserved populations. Thus, providing greater access to borrowings for more people-and greets a new door for the businesses.

Minimize Risks through AI

The major issue for lenders is loan default. Artificial Intelligence provides lenders with a stronger likelihood of identifying those borrowers who will likely default their loan. The traditional underwriting system primarily depends on past behavior that exists and is available. Contrary to this, AI fundamentally uses a set of many criteria wherein the assessment of the borrower's current financial capability is made. Unlike emphasizing a borrower based on his past performance an AI enables proper assessment of factors of risk assessment on the borrower.

AI-based systems continuously learn and adapt. It can be the real-time tracking of the profile of a borrower to identify early warning signs, which may include delayed payments or increased spending behavior. That way, lenders can point out problems early. PwC reports that for 2023, reports indicate AI has assisted banks in reducing nonperforming loans up to 30%. Financial problems are arrested before they become catastrophic for both lenders and borrowers.

What’s Next for AI in Lending?

AI is still new when it comes to credit scores and loan approvals, but it’s growing fast. In the future, we’ll see AI being used even more in the lending process. We might see more customer service chatbots and fully automated loan approvals.

One exciting development is AI’s ability to assess risk in real time. Some fintech companies are already using AI to keep an eye on borrowers’ financial health all the time. This lets lenders make quick decisions to reduce risks.

AI also has the potential to make lending fairer by reducing human biases. While AI isn’t perfect yet and there are still problems with biased data, many companies are working hard to make sure AI systems are fair and equal for everyone.